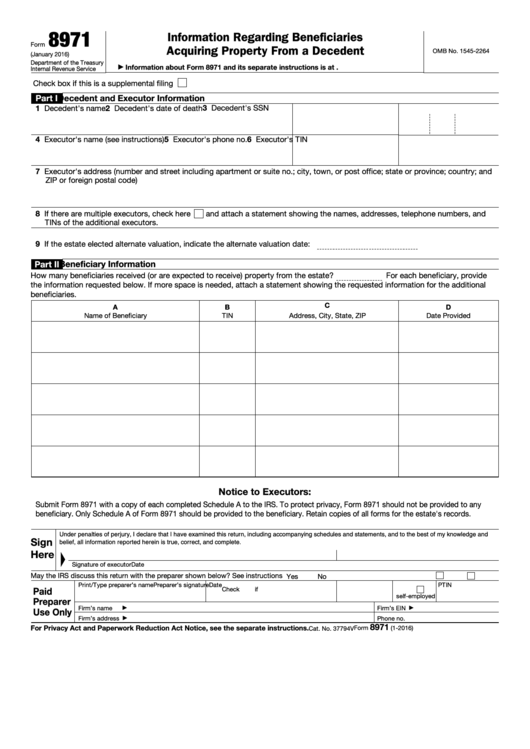

Form 8971 Instructions 2021

Form 8971 Instructions 2021 - Executor's name (see instructions) 5. Part i decedent and executor information. $260 per form 8971 (including all About form 8971, information regarding beneficiaries acquiring property from a decedent | internal revenue service Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. Web the irs has issued a new form 8971 “information regarding beneficiaries acquiring property from a decedent” and instructions. The maximum penalty is $532,000 per year (or $186,000 if the taxpayer qualifies for lower maximum penalties, as described below). Web form 8971 instructions pdf. The penalty is as follows. One schedule a is provided to each beneficiary receiving property from an estate.

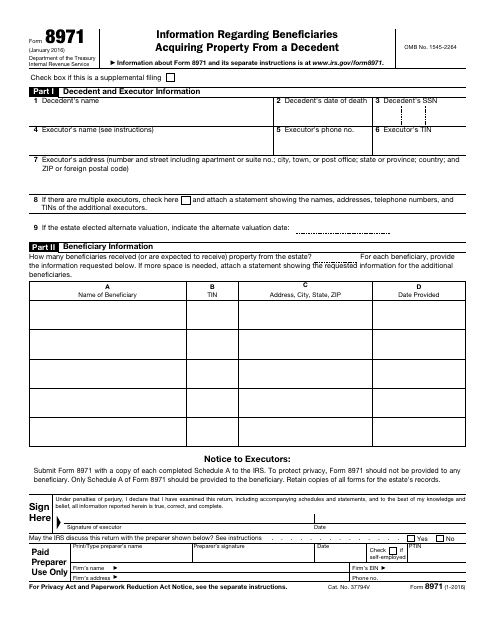

Part i decedent and executor information. The penalty is as follows. About form 8971, information regarding beneficiaries acquiring property from a decedent | internal revenue service Web when the correct form 8971 with schedule(s) a is filed. On march 2, 2016, the irs and treasury published proposed regulations regarding sections 1014(f) and 6035. This information return reports the values from the decedent’s gross estate to both the irs and to each beneficiary receiving property from the estate. $50 per form 8971 (including all schedule(s) a) if it is filed within 30 days after the due date. Form 8971 and attached schedule(s) a must be filed with the irs, separate from. Executor's name (see instructions) 5. Web form 8971 instructions pdf.

Check box if this is a supplemental filing. Executor's name (see instructions) 5. Web if you received a schedule a to form 8971 for property and part 2, column c, of the schedule a indicates that the property increased the estate tax liability, you will be required to report a basis consistent with the final estate tax value of the property reported in part 2, column e, of the schedule. The maximum penalty is $532,000 per year (or $186,000 if the taxpayer qualifies for lower maximum penalties, as described below). Web when the correct form 8971 with schedule(s) a is filed. On march 2, 2016, the irs and treasury published proposed regulations regarding sections 1014(f) and 6035. Form 8971 and attached schedule(s) a must be filed with the irs, separate from. Part i decedent and executor information. Web form 8971 and accompanying schedule a are used to fulfill the section 6035 reporting obligations to the irs and the beneficiaries of estates. The penalty is as follows.

IRS Form 8971 Instructions Reporting a Decedent's Property

Web form 8971 instructions pdf. Part i decedent and executor information. Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. Web when the correct form 8971 with schedule(s) a is filed. Web if you received a schedule a to form 8971 for property and part.

New IRS Form 8971 Rules to Report Beneficiary Cost Basis Fill Out and

Web form 8971 and accompanying schedule a are used to fulfill the section 6035 reporting obligations to the irs and the beneficiaries of estates. The penalty is as follows. This information return reports the values from the decedent’s gross estate to both the irs and to each beneficiary receiving property from the estate. Web the irs has issued a new.

Form 12277 Instructions 2021 2022 IRS Forms Zrivo

Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. Web if you received a schedule a to form 8971 for property and part 2, column c, of the schedule a indicates that the property increased the estate tax liability, you will be required to report.

2021 Form IRS Instructions 1120S Fill Online, Printable, Fillable

Form 8971 and attached schedule(s) a must be filed with the irs, separate from. Check box if this is a supplemental filing. Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. $260 per form 8971 (including all Web irs form 8971 is the tax form.

2020 2021 Irs Instructions Form Printable Fill Out Digital PDF Sample

Web this form, along with a copy of every schedule a, is used to report values to the irs. On march 2, 2016, the irs and treasury published proposed regulations regarding sections 1014(f) and 6035. This information return reports the values from the decedent’s gross estate to both the irs and to each beneficiary receiving property from the estate. Check.

New Basis Reporting Requirements for Estates Meeting Form 8971

Web form 8971 and accompanying schedule a are used to fulfill the section 6035 reporting obligations to the irs and the beneficiaries of estates. One schedule a is provided to each beneficiary receiving property from an estate. Web when the correct form 8971 with schedule(s) a is filed. Web this form, along with a copy of every schedule a, is.

IRS Form 8971 Instructions Reporting a Decedent's Property

Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. The maximum penalty is $532,000 per year (or $186,000 if the taxpayer qualifies for lower maximum penalties, as described below). The penalty is as follows. Web this form, along with a copy of every schedule a,.

IRS Form 8971 Instructions Reporting a Decedent's Property

$50 per form 8971 (including all schedule(s) a) if it is filed within 30 days after the due date. The penalty is as follows. Part i decedent and executor information. This information return reports the values from the decedent’s gross estate to both the irs and to each beneficiary receiving property from the estate. Form 8971 is required to be.

Fillable Form 8971 Information Regarding Beneficiaries Acquiring

$50 per form 8971 (including all schedule(s) a) if it is filed within 30 days after the due date. Web information about form 8971 and its separate instructions is at. Web this form, along with a copy of every schedule a, is used to report values to the irs. Web if you received a schedule a to form 8971 for.

IRS Form 8971 Download Fillable PDF or Fill Online Information

The penalty is as follows. Check box if this is a supplemental filing. $260 per form 8971 (including all Web form 8971 and accompanying schedule a are used to fulfill the section 6035 reporting obligations to the irs and the beneficiaries of estates. Web when the correct form 8971 with schedule(s) a is filed.

Web Form 8971 Instructions Pdf.

Form 8971 and attached schedule(s) a must be filed with the irs, separate from. Web form 8971 and accompanying schedule a are used to fulfill the section 6035 reporting obligations to the irs and the beneficiaries of estates. $260 per form 8971 (including all The maximum penalty is $532,000 per year (or $186,000 if the taxpayer qualifies for lower maximum penalties, as described below).

On March 2, 2016, The Irs And Treasury Published Proposed Regulations Regarding Sections 1014(F) And 6035.

Web information about form 8971 and its separate instructions is at. Web if you received a schedule a to form 8971 for property and part 2, column c, of the schedule a indicates that the property increased the estate tax liability, you will be required to report a basis consistent with the final estate tax value of the property reported in part 2, column e, of the schedule. Executor's name (see instructions) 5. Web this form, along with a copy of every schedule a, is used to report values to the irs.

This Information Return Reports The Values From The Decedent’s Gross Estate To Both The Irs And To Each Beneficiary Receiving Property From The Estate.

Part i decedent and executor information. Check box if this is a supplemental filing. Web irs form 8971 is the tax form that the executor of an estate must use to report the final estate tax value of property of that estate. Web when the correct form 8971 with schedule(s) a is filed.

The Penalty Is As Follows.

This increases the duties of a personal representative or executor of a decedent’s estate. Form 8971 is required to be filed if an estate has to file an estate tax return under form 706 after july 31, 2015. $50 per form 8971 (including all schedule(s) a) if it is filed within 30 days after the due date. One schedule a is provided to each beneficiary receiving property from an estate.